|

A Sign of Things to Come? (See on-line version in the Austrian Economics Newsletter) Roger

W. Garrison

My official duties were to conduct three seminars on successive Tuesdays (May 27, June 3, and June 10) and to deliver LSE's first Hayek Memorial Lecture on the evening of June 5. Stemming from these activities, however, were a number of other opportunities and developments, including a visit to No. 10 Downing, a meeting with Lord Skidelsky at Westminster's Millbank House, an article in ama-gi, the journal of the LSE Hayek Society, an interview for Enclave and for internet outlets, and more. All in all, I see the LSE visit as a step towards regaining the visibility of the Austrian School in an institution where this school once thrived. Pre-publicity in ama-gi

Three Seminars

As it turned out, the presentation was well received, as indicated by the discussion that followed and by the next day's e-mail. Hubert Strecker, who had come from the University of Copenhagen to attend the seminar, wrote that although he had read Chapters 3 and 4 of my book, the seminar gave him some new ideas about capital-based macroeconomics. He returned from Copenhagen for the second and third seminars and visited me in my office after the final lecture to discuss aspects of my book that were of special interest to him. Mr. Strecker had chosen the Austrian theory of the business cycle for his thesis topic. Another participant, Ms. Krisztina Majoros of the University of Miskolc (Hungary), was doing research on Tibor Scitovsky, who was a student at LSE when Hayek and Keynes (of King's College, Cambridge) were vying for the attention of promising students. I was able to call her attention to an interview with Scitovsky published by David Colander and Harry Landreth in their The Coming of Keynesianism to America (Edward Elgar, 1996). Scitovsky's reaction to the Austrian theory was typical: "Hayek was the only member of the faculty to have an explanation for the depression; but his two books on the business cycle seemed too convoluted and confusing to carry conviction." Scitovsky was looking for "an altogether new and different approach" and soon found it in Keynes's General Theory. The Austrians have always had an up-hill battle in conveying ideas about business cycles in a framework that incorporates the capital theory of Eugen von Böhm-Bawerk. Keynesian theory is easier to learn and comes with a full complement of policy prescriptions to boot. The second seminar attracted the same group plus a few others. The objective in this session was to put Hayek and Keynes head-to-head in such a way that the critical differences in their respective macroeconomic frameworks became transparent. Abba Lerner, in an interview included in the Colander-Landreth volume, had pin-pointed early on a key difference in terms of relative movements of consumption and investment: For classical economists [including Hayek], consumption and investment are alternative ways of allocating resources. The two magnitudes move in opposite directions under conditions of binding resource constraints. For Keynes, resource constraints are generally not binding and the two magnitudes move up and down together. In Time and Money, this contrast takes the graphical form of movements along a production possibilities frontier (for Hayek) and movements away from and towards the frontier (for Keynes). Here we have a contrast between an economy that can accommodate changing market conditions and an economy that is inherently dysfunctional in the face of any change. The analytics underlying this contrast entail a capital structure whose temporal profile can be altered (Hayek) and a capital structure for which only the degree of utilization can vary (Keynes). My graphical exposition consisted of (1) showing how the economy would work under the restrictive and debilitating Keynesian assumptions and then (2) relaxing these assumptions to let the dysfunctional Keynesian economy morph into a fully functional Hayekian economy. The intent was to make the participants wonder why Keynes had omitted from his theory the very market mechanisms that are essential for keeping production activities in line with consumption preferences. So presented, Hayek's theorywith Austrian capital theory in playdoes not in the least seem convoluted, while Keynes's theory, with no capital theory at all, seems eviscerated. The third seminar, which dealt with monetarism and subsequent developments in macroeconomics, gave me an opportunity to respond to questions raised in earlier sessions or submitted to me by e-mail. Andy Denis, a faculty member of London's City University, had wondered if Hayekian theory could properly be considered to be macroeconomics. Citing page 293 of Keynes's General Theory, Professor Denis asked if the Austrians reject the conception of macroeconomics as "the Theory of Output and Employment as a whole"? Here was my chance to deal with the status of macroeconomics in Austrian economics and to say something about the issue of aggregation. The Austrians use the term macroeconomics to refer to a set of substantive issuesto economywide phenomena such as inflation, deflation, widespread unemployment and business cycles. Keynes's "output as a whole" and the constituent aggregates of consumption and investment have a claim on his attention because of their perverse movements in circumstances of changing market conditions. For instance, an inclination on the part of income earners to save more sends output and employment spiralling downward until actual saving is brought into balance with some given level of investment. The economy's one-dimensional measure of performance (output) is at the same time the adjustment mechanism that keeps saving in line with investment. To conceive of macroeconomics as the theory of this measure-of-performance-cum-adjustment-mechanism is virtually to build perversity into macroeconomics at the definitional level. Also, the suitability of the chosen macroeconomic aggregates comes into question here. Keynes operated at a level of aggregation where he could see a big problem (the difficulty of coordinating saving and investment) but could not see any non-perverse market solution. As an essential stratagem for countering Keynes, the monetarists increased the level of aggregation, effectively covering up the problem by giving little or no play to the constituent aggregates of consumption and investment. Consumption (C) and investment (I) were simply combined into aggregate output (Q), which then appears in the monetarists' equation of exchange (MV=PQ). The absence of capital theory in monetarist thinking precluded any satisfactory understanding of the issues raised by Keynes. The Austrians have always insisted on a decreased level of aggregationwith the investment aggregate made up of temporally sequenced stages of production. Their aggregation scheme is more appropriate to the problem at hand. It allows them to see both the problem emphasized by Keynes and a non-perverse market solution to that problem. An Interview for Enclave

We spent an hour or so in my office. Our questions-and-answer session, which I very much enjoyed, was all recorded for later transcription and editing. A week or so later Massimiliano sent me the edited transcription for further editing by me. I was pleased with the result and especially pleased to go on record with the story of the origins and subsequent exhumation of Milton Friedman's "plucking model"his graphical description of movements in aggregate output and employment which are supposedly telling against the Austrians. Massimiliano is preparing the interview for posting in both English and Italian on two web sites; US Equity & Macro LAB and Liberanimus Institute and is pleased to have it posted on the Mises Institute's site as well. An Italian translation of selected portions of the interview along with Massimiliano's account of the seminar series will appear in Enclave, a prominent Italian libertarian magazine. LSE's Hayek Memorial Lecture

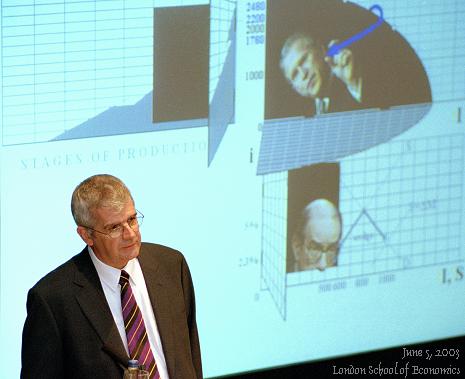

I began thinking about using some photographs of Hayek (PHOTO #1; PHOTO #2), some of which I had taken in the 1970s while Hayek was in residence at the Institute for Humane Studies in Menlo Park, California. A few days later I went to lunch with Tim Besley, Toby Baxendale, and Reggie Simpson. (Reggie, who was from LSE's Office of Development and Alumni Relations, looked after every detail during the planning phase of the June 5 events, which included not only the lecture but also a dinner in the Senior Dining Room with 16 invited guests.) I mentioned to Toby that I had prepared my lecture but that I might want to use the large screen for photographs. Toby seemed a little surprised, saying that surely I would use the screen for the graphical treatment of Hayekian macroeconomics, which forms the core of my book. "That's your contribution, isn't it?" I had been hesitant to incorporate the graphical exposition into the lecture, thinking that the evening audience might not warm up to the macro-analytics of the business cycle. But with Toby's encouragement, I scrapped most of my prepared lecture and began to rewrite around the graphics. I pared down my PowerPoint file, replacing most all of the explanatory notes with pithy Hayek quotations and paraphrasings. I added some photographs of Hayekand of Keynesto help keep the story straight. I left in the few cameo appearances of Greenspan, Clinton, and Bush that had always worked well with Auburn students. Though radically changed, the lecture still fit the title pretty wellsince most all of Hayek's contributions to economics come together in the Mises-Hayek theory of the business cycle. I mentioned to several people about how I had changed my lecture plan and was warned by a few not to confront this audience with graphical analysis. But it was too late. I had to deliver a final copy of the PowerPoint file to the audio-visual people several days before the lecture. At that point there was no scope for changes of any kind. On the evening of June 5, I arrived at the Old Theatre a little early to meet Tony Giddens, the widely known sociologist and the Director of LSE. He was to do the introduction. I was pleased to see that an audience was arriving, too. Though the lecture was well publicized, none of us had any idea of just how many might actually choose to attend this first Hayek Memorial Lecture. By six o'clock, the auditorium was filling up. Some 300 to 350 people, it turned out, had an interest in hearing about Hayek. Professor Giddens was a gracious host for the evening. In his introductory remarks, he oversold the lecture in a humorous way and then focussed the audience's attention to the dispute between Hayek and Keynes, quipping in a muted voice that he would probably come down on the side of Keynes. Unknowingly, he set himself up for a mild chiding: I expressed enthusiasm for being invited to give a lecture on LSE's star professor of the 1930s and 1940s and then complained that the Director had scheduled this Hayek lecture on Keynes birthday! But I couldn't mention that coincidence of dates without also mentioning that Keynes shared his birthday with none other than Adam Smithwhich allowed me to segue back to Hayek. The lecture worked for me. The audio-visual aspects came off without

a hitch. And the message was well received. It was not difficult to establish

that Keynes saw no way for the market to work. Increased saving, Brief discussions with members of the audience immediately after the lecture were gratifying. The various reactions made me realize just how diverse the audience was. One gentleman wanted to discuss further Keynes's and Hayek's views on interest-rate theoryand we did discuss that issue in a subsequent exchange of e-mails. One woman (I regret not getting her name) expressed great pleasure in hearing my lecture and then told me she was a student of Hayek's and Robbins' in 1947. One young Hayek enthusiast, who I later learned was Espen Bardsen, a Norwegian professional football player who played 1st class football for the London team Tottenham Hotspurs (Premier League) and played for his country in international competition, handed me a copy of a recent Federal Reserve document titled "Monetary Policy in a Zero-Interest-Rate Economy" It was a strategy paper that addressed the prospects of the Fed's adopting extraordinary means in its efforts to stave off a deflation. The dinner that followed in the Senior Dining Room was a memorable event for me. The guest list included Ken Minogue, LSE Professor of Politics, and Razeen Sally, LSE Senrior Lecturer in International Political Economy. Professor Sally had recently written an article for ama-gi on "Hayek and the International Order." Ralph Raico, who wrote under Hayek at the University of Chicago and is now Professor of European History at the State University of New York, had flown into London for the occasion. Also in attendance was Sven Folkesson, President of the LSE Hayek Society. Tony Giddens moderated a lively discussion among the diners, and I was made to feel that Hayekian ideas were back in the air at LSE. A Visit at No. 10 Downing

What struck me during the visit at No. 10and I hope it struck Mr. Scott, toois that the story as told by an academic economist and as told by a real live entrepreneur/businessman were in perfect harmony. I've become aware over the years that this is a characteristic of Austrian economics that cannot be matched by other schools of macroeconomic thought. Hayek's ideas ring true in the financial and business community in ways that the "rational expectations" of new classicism or the "menu costs" of new Keynesianism do not. Credit expansion gives us an artificial boom. Rock-bottom interest rates after the bust forestalls a genuine recovery. The Federal Reserve's near-phobic resistance to any price or wage decreases reflect its resolve not to repeat the blunders of the 1930s. But avoiding a deep depression has gotten translated into precluding a timely correction. The Fed, in effect, is trading depth for duration. The shallow recession drags on. We made it clear that in the final analysis the Austrian theory suggests banking reform and not just some alternative policy prescription for adjusting interest rates. The reform measure currently on the table in Britain would be a dramatic one. Britain could join the Eurosystem, the Bank of England relinquishing key powers to the European Central Bank. Mr. Scott put into perspective for us the recent choice by Tony Blair to postpone for now making any decision to abandon the pound for the euro. The implications of Austrian theory about the advisability of Britain's adopting the euro are mixed. Generally, Austrian economists favor reform in the direction of decentralization. Clearly, expanding the Eurosystem to include Britain would be a move in the opposite direction. But, Austrian economists also favor putting monetary decisions in the hands of those least likely to use it for narrow political purposes. In recent years, the Bank of England has constrained itself to rule-following behaviorcertainly more so than has the Federal Reserve. But in the past it has not been above using its discretionary powers to serve the interests of an incumbent administration. Nor is there any firm institutional check against such politicisation in the future. It is worth pointing out that relinquishing control of monetary matters to the European Central Bank would effectively eliminate political business cyclesor, at least, ones with British origins. And without an accommodating central bank, the British treasury, like the treasuries of the other euro-using countries, would be put on a shorter leash. The down side of Britain adopting the euro is the inherent problems of centralization. As is well known by seasoned Fed watchers, blunders committed by a central bank can have dramatic and far-reaching consequences. So, while the European Central bank is relatively well insulated from the narrow political interests of its euro-using members, those member nations are continuously exposed to the potential ineptness or miscalculation that tends to characterize any organization not subject to the discipline of the marketplace. In the end, this consideration, an implication of socialist-calculation debate, may be an overriding one. A breakfast meeting between Toby Baxendale and Derek Scott subsequent to our June 12 meeting at No. 10 and after I had departed for the United States evidenced a continuing interest in Hayekian ideas and their implications for policy prescription and institutional reform. A Meeting with Lord Skidelsky

at Westminster's Millbank House

High on my "must-do" list was a meeting with Professor Skidelsky. I was convinced that my own graphical rendition of Keynes's analytical framework in Time and Money is truer to Keynes than is the conventional IS-LM model or the Aggregate-Supply/Aggregate-Demand construction. My confidence in this judgment was bolstered when I read the second volume of Skidelsky's biography. My pictures go well with his story. Near the end of my stay at LSE, I e-mailed Professor Skidelsky, hoping to make a quick trip to Cambridge for a visit. He replied promptly and indicated that he would be spending the following week in London and that he would be pleased to see me at the Millbank House. As instructed, I phoned his assistant and made arrangements for the visit. Westminster's Millbank House, an ornate red-brick office building, overlooks Victoria Tower Gardens, which are adjacent to the Parliament building. I arrived there for my visit mid-morning on June 17. I was announced and was soon greeted in the lobby by Lord Skidelsky. We walked to a near-by dining room where we could have coffee and visit. Lord Skidelsky had been immersed in the study of the Russian language but was happy to take a break to talk macroeconomics. I was pleasantly surprised to learn that he had read key portions of my Time and Money. And we seemed to be in substantial agreement about the fundamental differences between Keynes and Hayek. Lord Skidelsky was able to add a human touchmaybe just a good biographer's touchto the lingering question of why Hayek didn't review the General Theory: "He just wasn't up for another mauling by the Keynesians." By the time his 1936 book was in print, Keynes's coterie of disciples was well formed and ready to do battle with any and all nay-sayers. The vitriolic attacks that had been provoked by Hayek's earlier review essay on Keynes's Treatise on Money would undoubtedly have been replayed in spades. Keynes's far-reaching influence in both academic and political circles together with the politically attractive policy implication of his theory made the contest between Keynes and Hayek a very lop-sided one. I have always believed that understanding Keynes's views on the economy requires that we understand Keynes's view of himself. In his biography, Lord Skidelsky found it almost too obvious to mention that the title of Keynes's book was cribbed from Einstein. Calling it The General Theory was not intended to suggest, as some Keynes scholars would have us believe, that the book is mostly about theory and not really about policy. Nor did the title signal an abandonment of Marshallian partial-equilibrium analysis in favor of some Walrasian or Casselian general-equilibrium analysis. Rather it not-to-cryptically suggested just where the author of the General Theory stood in relationship to all other economists, living and dead. When I returned to LSE and with our discussion of Keynes and Einstein still on my mind, I pulled a copy of Skidelsky's Volume II from the shelf to remind myself that the significance of Keynes's title was actually well known at the time the book came out. Skidelsky quotes from Cecil Pigou's 1937 review: "Einstein actually did for Physics what Mr. Keynes believes himself to have done for Economics." Skidelsky has provided a double service here: A long-forgotten but telling insight has been revived, and the enduring value of keeping the history of economic thought alive has once again been demonstrated. A Full Five Weeks

I can hope that in Austrian circles the year 2003 will be remembered as the year that Hayekian economics returned to LSE. Keynesianism there, like elsewhere, has become splintered into sub-schools, and mainstream macroeconomics in general seems to have no cutting edge. But LSE has good students, and it has an unequaled reputation for placing graduates in influential positions around the world. Other Hayek Visiting Fellows in the years ahead and possibly an ongoing Hayek program can turn the 2003 visit into the start of something grand.

|

It was my privilege

to be the first Hayek Visiting Fellow at the London School of Economics.

The five-week visit during May/June 2003, hopefully to be followed by other

such visits in the years ahead, was co-sponsored by LSE and the

It was my privilege

to be the first Hayek Visiting Fellow at the London School of Economics.

The five-week visit during May/June 2003, hopefully to be followed by other

such visits in the years ahead, was co-sponsored by LSE and the  capital-based

macroeconomics. This graphical presentation draws heavily from the core

chapters (Chs. 3 and 4) of my

capital-based

macroeconomics. This graphical presentation draws heavily from the core

chapters (Chs. 3 and 4) of my

for

instance, would not finance increased investment but rather would send

the economy into recession. The attempt to save would be aborted in the

face of decreasing incomes. Keynes's Paradox of Thrift was a profound denial

of even the possibility that the market might coordinate the plans of producers

with the decisions of savers. Hayek showed just why Keynes "saw no way":

he had no capital theory. We have to add Bohm-Bawerk's capital theory,

allow for differential interest-rate effects within the capital structure,

and acknowledge the existence of real, live entrepreneurs. These are the

amendments that make Keynesianism morph into Austrianism. With this audience,

putting the Hayekian graphics through their paces as the story was told

had the intended effects. It was easy to come down on the side of Hayek.

The economy is sent into recession not by some ill-fated attempt by workers

to save more but by an ill-advised attempt of the central bank to stimulate

more growth than savers are willing to finance. Further, the central bank's

attempts to re-ignite the boom after the bust has come is more likely to

postpone a genuine recovery than to hasten it. If Keynes won the day against

Hayek, it was because of the political popularity of his policy prescriptions

and not because of the cogency of his theorizing.

for

instance, would not finance increased investment but rather would send

the economy into recession. The attempt to save would be aborted in the

face of decreasing incomes. Keynes's Paradox of Thrift was a profound denial

of even the possibility that the market might coordinate the plans of producers

with the decisions of savers. Hayek showed just why Keynes "saw no way":

he had no capital theory. We have to add Bohm-Bawerk's capital theory,

allow for differential interest-rate effects within the capital structure,

and acknowledge the existence of real, live entrepreneurs. These are the

amendments that make Keynesianism morph into Austrianism. With this audience,

putting the Hayekian graphics through their paces as the story was told

had the intended effects. It was easy to come down on the side of Hayek.

The economy is sent into recession not by some ill-fated attempt by workers

to save more but by an ill-advised attempt of the central bank to stimulate

more growth than savers are willing to finance. Further, the central bank's

attempts to re-ignite the boom after the bust has come is more likely to

postpone a genuine recovery than to hasten it. If Keynes won the day against

Hayek, it was because of the political popularity of his policy prescriptions

and not because of the cogency of his theorizing.